Order by August 31, 2024 and receive a 10% discount on PRINTED Tax and Financial Planning Guides

Featured products

-

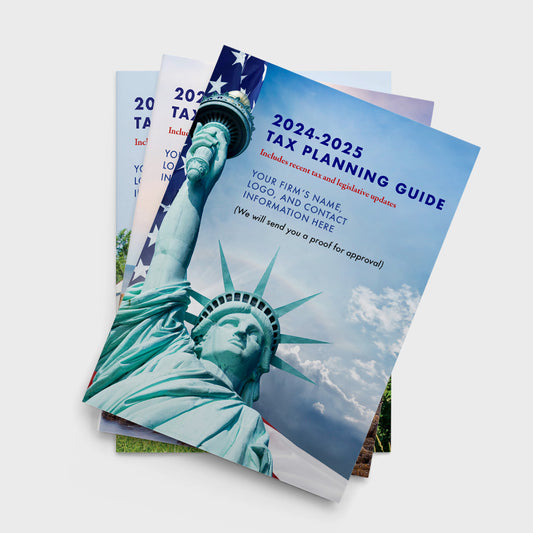

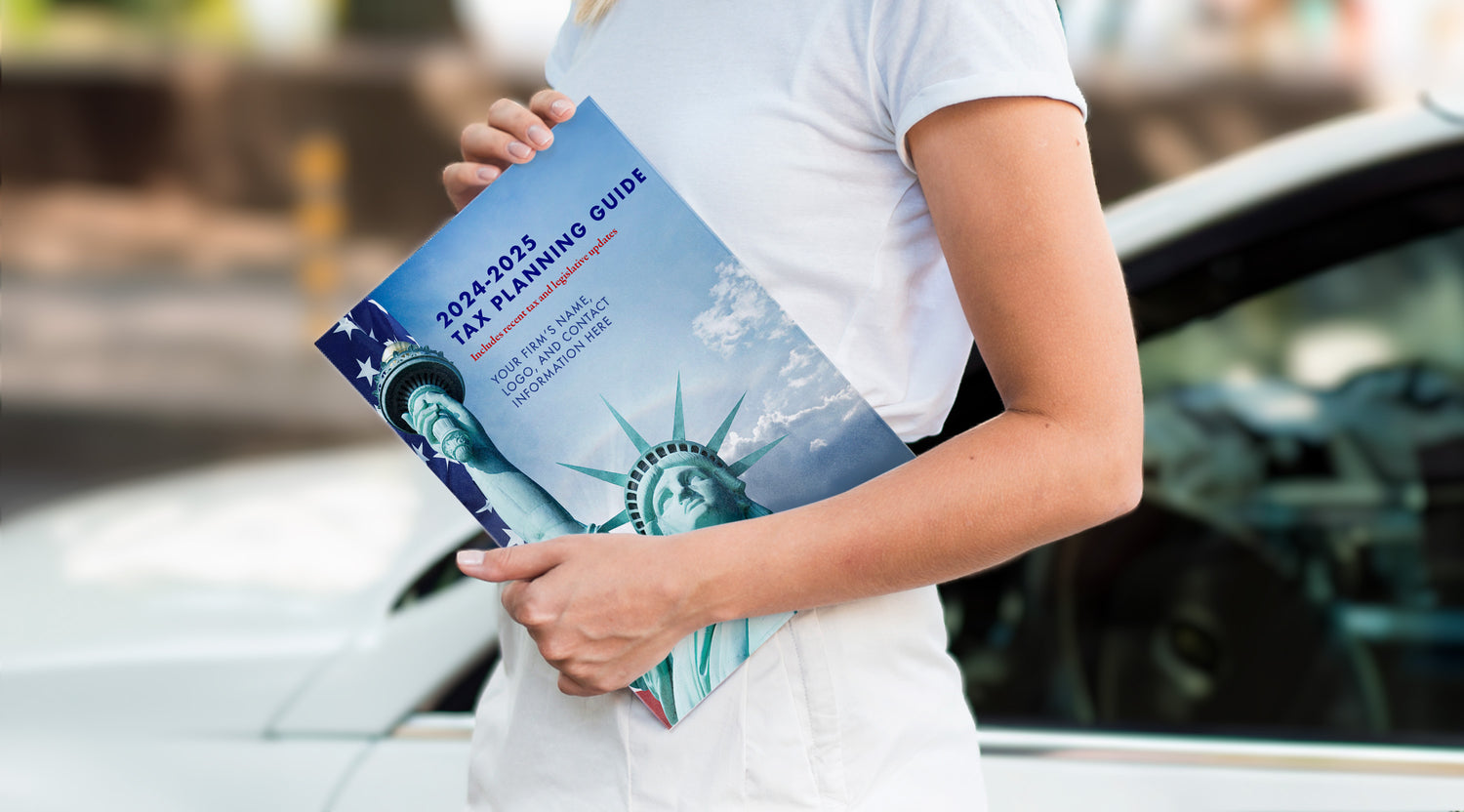

Large Tax Planning Guide

Regular price From $3.55 USDRegular priceUnit price per -

9x12 Envelope For Large Tax Planning Guide

Regular price $0.59 USDRegular priceUnit price per -

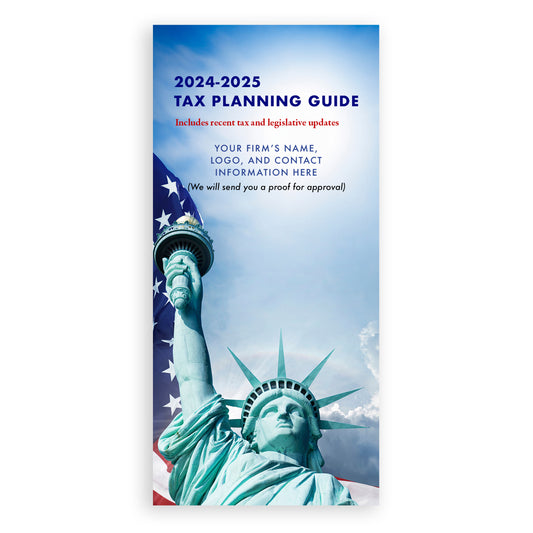

Small Tax Planning Guide

Regular price From $3.10 USDRegular priceUnit price per -

#10 Envelope For Small Tax Planning Guide

Regular price $0.43 USDRegular priceUnit price per -

Printing Options for Tax Planning Guide Inside Covers

Regular price $0.30 USDRegular priceUnit price per -

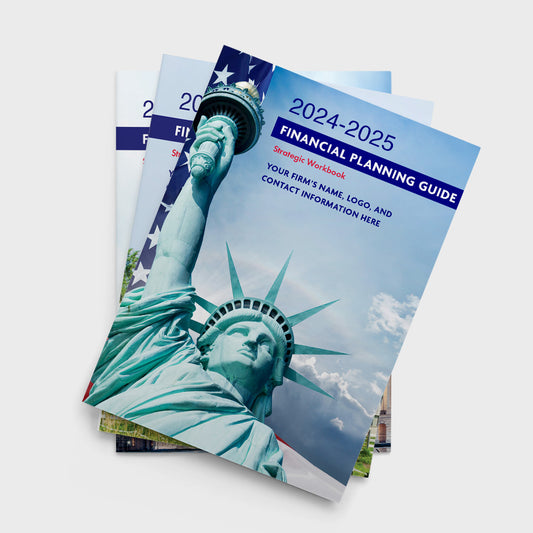

Financial Planning Guide

Regular price From $3.45 USDRegular priceUnit price per -

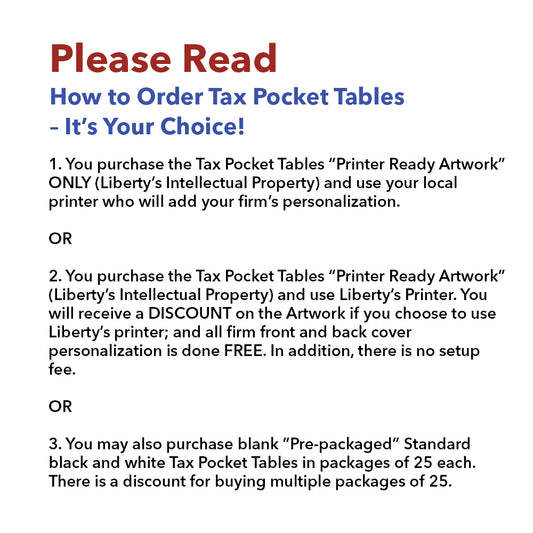

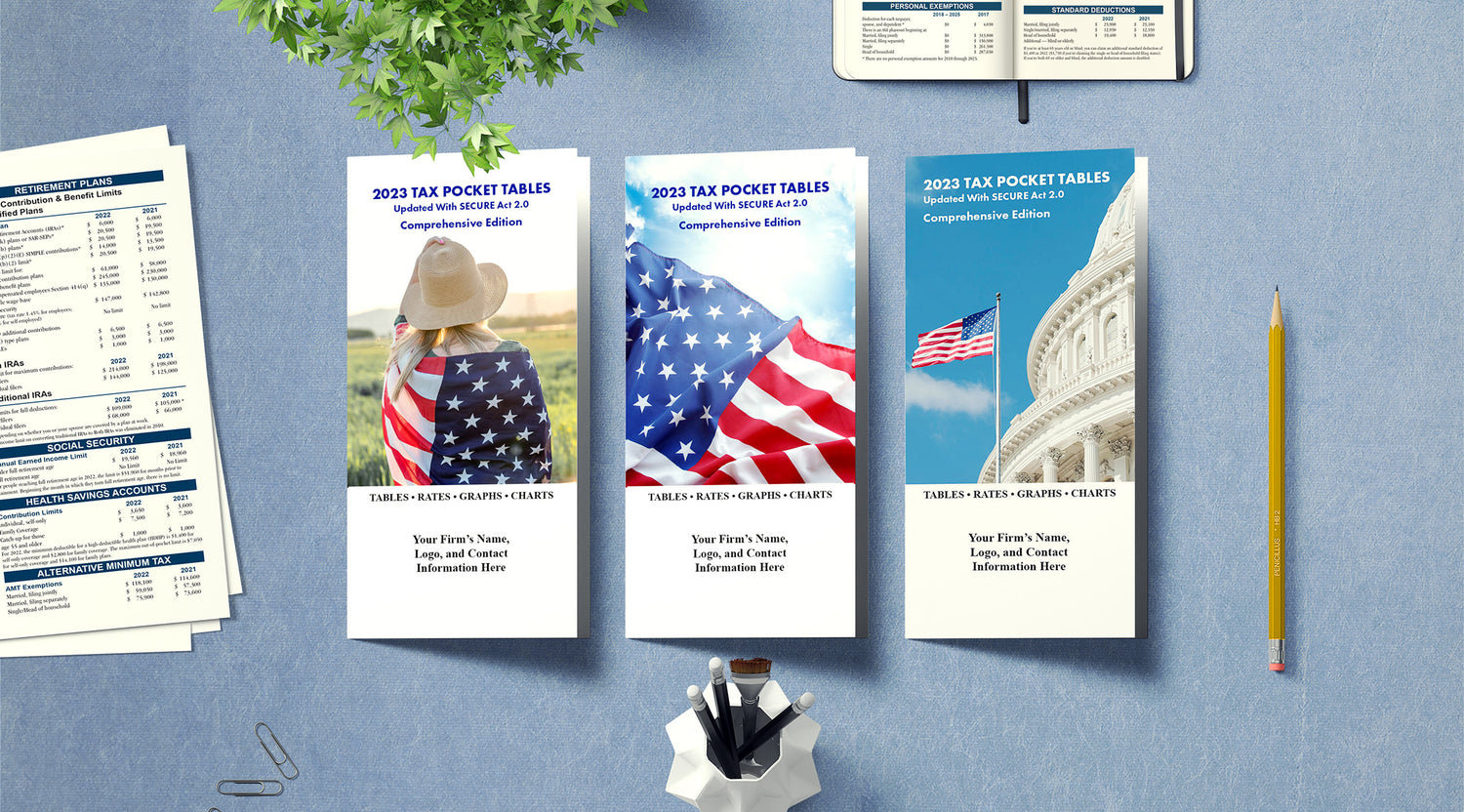

Standard Tax Pocket Tables

Regular price From $1.15 USDRegular priceUnit price per -

Tax Planning Guide “Page Turning” PDFs Without Printed Guides

Regular price From $499.00 USDRegular priceUnit price per